Car Affordability by Income: Why a $100,000 Salary Doesn’t Automatically Mean a $1,000 Car Payment

A realistic car payment is often discussed as a percentage of income, but salary alone never tells the full story. A $100,000 income may make a $1,000 payment look reasonable on paper, yet lenders and consumers still need to consider debt-to-income ratio, payment-to-income ratio, credit profile, and the full cost of owning the vehicle before calling that payment affordable.

If there is one takeaway here, it is this: approval and affordability are not the same thing. You may be able to qualify for a payment that still leaves too little room for savings, emergencies, housing, childcare, or rising everyday expenses. That is exactly why the smarter question is not “What car payment can I get approved for?” but “What car payment still leaves room for life?”

Why income alone doesn’t determine an affordable car payment

Equifax is especially clear on one point many buyers misunderstand: income generally is not a factor used to calculate credit scores, and it is not included in your credit report. Lenders may still consider your income, with your permission, when evaluating applications for credit such as auto loans, but earning more money does not automatically raise your credit score or prove a high payment is wise.

Equifax also explains that lenders use credit scores alongside other information from the application process, including things like income, residence history, and banking relationships. In other words, credit score measures credit behaviour, while affordability measures whether the payment actually fits your real budget.

What lenders look at besides credit score

TransUnion says there is no standard minimum credit score to be approved for a car loan. Approval depends on the lender, the type of sale, and other financial factors, including your income and how much debt you already have. That matters because it undercuts the idea that one salary figure should automatically map to one “safe” car payment.

TransUnion’s auto-financing guidance also says most lenders prefer a debt-to-income ratio (DTI) of 36% or lower. DTI compares your total monthly debt obligations with your gross monthly income, which means a buyer with student loans, rent, credit card balances, or childcare costs may have far less room for a car payment than salary alone suggests.

On top of DTI, TransUnion says some lenders look at payment-to-income ratio (PTI) and may want the car payment itself to stay around 15% to 20% of monthly income. That is a powerful reminder that even for a six-figure earner, the “right” payment depends on what else is already committed each month.

Equifax makes the same broader affordability point from the lender side. In its auto-loan delinquency guidance, it says affordability means whether a consumer’s income can cover expenses, including debts, and that lenders should evaluate debts, income, loan-to-value ratios, and credit scores together when assessing repayment ability.

A practical 10%–15% rule for car payments

As a general budgeting rule of thumb, many shoppers use 10% to 15% of gross monthly income as a workable range for the car payment itself. That is not an official TransUnion or Equifax rule, but it fits neatly with TransUnion’s PTI discussion, which notes that some lenders cap PTI at 15% to 20%. In practice, 10% is the more conservative zone, while 15% is a more aggressive upper range that leaves less room for insurance, fuel, repairs, and other obligations. TransUnion

Car payment by income: comparison table

Using gross monthly income, here is a simple benchmark table:

| Annual Income | Gross Monthly Income | 10% Guideline | 15% Guideline | Practical takeaway |

|---|---|---|---|---|

| $40,000 | $3,333 | $333/mo | $500/mo | Safer to stay near the low end |

| $60,000 | $5,000 | $500/mo | $750/mo | Reasonable range depends on other debts |

| $80,000 | $6,667 | $667/mo | $1,000/mo | A $1,000 payment is possible, but not automatic |

| $100,000 | $8,333 | $833/mo | $1,250/mo | $1,000 is around 12% of gross income |

| $150,000 | $12,500 | $1,250/mo | $1,875/mo | Higher income still needs debt review |

What this table shows is simple: a person making $100,000 per year does not automatically “deserve” or comfortably afford a $1,000 monthly car payment. It falls between the conservative and aggressive guideline zones, but whether it is truly affordable depends on DTI, PTI, and the rest of the household budget.

Why a $100,000 salary still doesn’t guarantee a safe $1,000 car payment

On paper, the math can look fine. A $100,000 salary equals roughly $8,333 in gross monthly income, so a $1,000 payment comes out to about 12% of gross pay. That does not automatically make it reckless, but it also does not automatically make it safe.

The bigger problem is that a car payment is never the full transportation budget. TransUnion tells shoppers to look beyond the loan payment and include taxes and fees, registration, gas, insurance, maintenance, tolls, parking passes, and tickets. A $1,000 payment is therefore not really a $1,000 transportation cost.

Equifax’s affordability framing supports the same conclusion. If affordability means whether income can cover expenses and debts, then a borrower with a strong salary but heavy rent, student loans, credit card balances, or childcare costs may be far more stretched than their income alone suggests.

How credit score affects car affordability

Credit score still matters, just not in the way many shoppers think. TransUnion says there is no universal minimum score for a car loan, but a stronger score can improve approval odds and reduce borrowing cost. It also notes that even a small rate difference can add up to hundreds or thousands of dollars over the life of the loan.

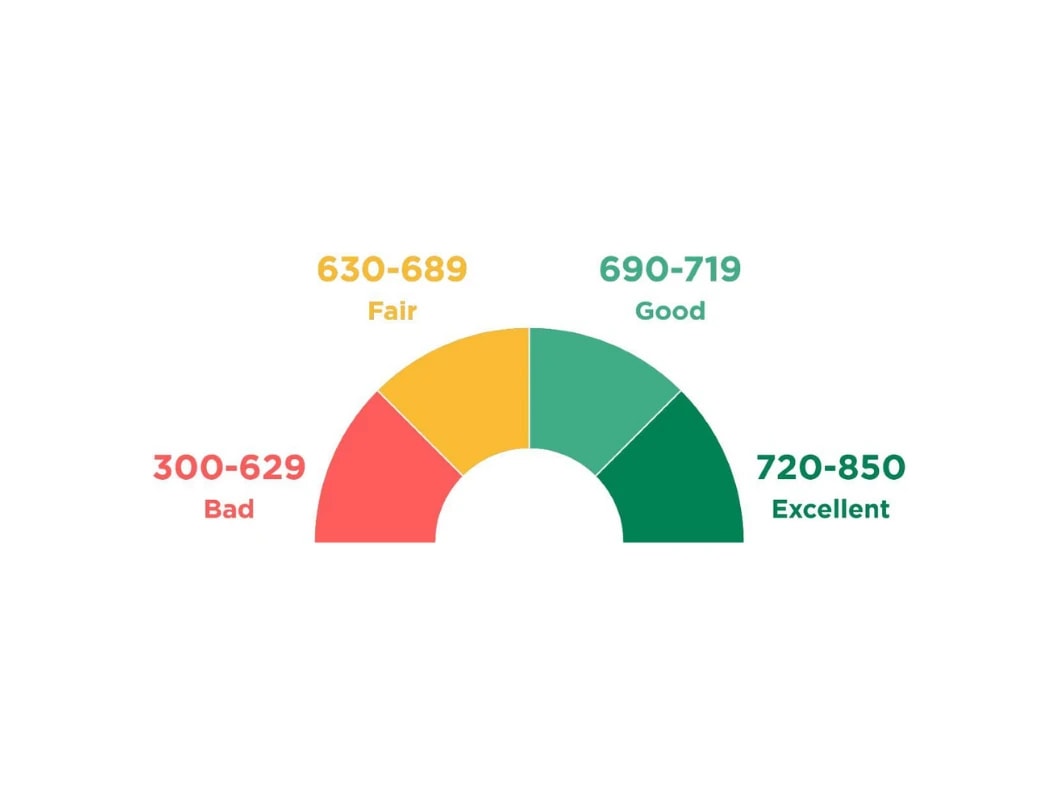

Score labels also depend on the model being used, so blogs should avoid treating one threshold as universal. Equifax’s general education pages list common ranges as 800–850 excellent, 740–799 very good, 670–739 good, 580–669 fair, and 300–579 poor, while its VantageScore 3.0 age page uses different VantageScore-specific bands. TransUnion’s direct-to-consumer VantageScore 3.0 guidance also uses its own labelling, calling 721–780 “good.” The takeaway is simple: always ask which scoring model is being referenced.

For context, Equifax says the average U.S. credit score was 701 on one education page and 705 on its state-by-state page using VantageScore 3.0 data from March 2024. It also says average scores by generation were 679 for Gen Z, 680 for Millennials, 700 for Gen X, and 742 for Baby Boomers as of September 2024. That helps explain why many shoppers are not entering the market with the kind of elite score profile that usually gets the best rates.

Today’s auto market makes affordability harder

The latest official TransUnion auto snapshot available at the time of writing is its Q4 2025 Credit Industry Insights Report, which says average monthly payments reached $782 for new vehicles and $538 for used vehicles. Average amounts financed climbed to $44,495 for new and $27,278 for used, while auto accounts 60+ days past due reached 1.50%.

TransUnion’s Q3 2025 report tells a similar story, with average monthly payments at $769 new and $538 used, and average financed amounts of $43,718 and $27,037 respectively. It also reported that the super prime tier represented 40.9% of consumers, while subprime represented 14.4%, reinforcing how the market is splitting between the strongest borrowers and everyone else.

Equifax’s recent commentary lines up with that pressure. One official article says affordability has been a challenge with average new-car payments around $766 monthly and used-car listings near $27,000, while a 2026 market update says average vehicle prices are now above $50,000 and affordability remains difficult.

Affordability stress has real consequences. Equifax says rising delinquency levels in credit card and auto loans point to affordability challenges, and TransUnion’s 2026 forecast expects auto accounts 60+ days past due to reach 1.54%, marking another year of elevated stress.

A quick word on subprime trends

If you want to understand how much pressure still exists in the market, Equifax’s January 2026 originations report shows that through October 2025, 18.0% of auto loan originations went to consumers with a VantageScore 3.0 below 620, accounting for 14.5% of origination balances. The average origination amount was $32,943 for all auto loans and $26,982 for subprime auto loans. Equifax report

Inflation and household pressure still matter

TransUnion’s latest Consumer Pulse Study says 48% of consumers expected income to increase in the next year, down from 53% a year earlier, while 43% expected income to stay the same. It also found that only 26% of households earning under $50,000 and 36% of households earning $50,000 to $99,999 felt their incomes kept up with inflation, compared with 45% of high-income households. TransUnion

That matters because a car payment competes with everything else in the household budget. The same study found that 81% of consumers listed inflation as a top three financial concern, which helps explain why a payment that looks manageable in a spreadsheet may feel much heavier in real life.

How to search by budget on AutoBandit

If you want to shop more realistically, start with your payment target and filter inventory to match it. On AutoBandit’s deals page, shoppers can use the Monthly Budget filter in the search area or the left sidebar to narrow the inventory to vehicles that fit a target payment. I verified that the public deals page includes this filter.

From there, choose the monthly budget range that fits your plan, such as under $300, $301 to $500, $501 to $750, $751 to $1,000, or above $1,000. Once you select a range, the page refreshes and shows vehicles within that payment band. For shoppers trying to avoid payment shock, this is a much smarter way to browse than starting with a dream model and hoping the numbers work later.

Signs your car payment is probably too high

A car payment should raise concern if it pushes you above roughly 15% of gross monthly income, if you need an unusually long loan term just to make the payment feel manageable, or if the payment leaves you unable to save consistently after covering essentials. Those are all warning signs that the car may fit the loan approval box better than the real-life budget box.

Another red flag is ignoring the rest of the ownership cost. If you are only thinking about the monthly note and not factoring in insurance, fuel, registration, maintenance, parking, and taxes, you are probably underestimating the true cost of the car.

How to lower your payment without overextending your budget

The fastest way to improve affordability is usually to choose a less expensive vehicle. A smaller purchase price often does more for your budget than trying to “engineer” an affordable-looking payment through a longer term.

It can also help to make a larger down payment, improve your credit before applying, and compare financing offers from multiple lenders instead of accepting the first quote. Better credit can reduce APR, and a lower APR can materially change both the monthly payment and the total cost over the life of the loan.

FAQ: Car affordability by income

How much car payment can I afford on a $100,000 salary?

Using a practical 10% to 15% guideline, a $100,000 income points to roughly $833 to $1,250 per month before insurance, fuel, maintenance, and existing debt are considered. Whether that is truly affordable depends on DTI, PTI, and your overall monthly obligations.

Is a $1,000 car payment too much?

It depends. For some households it may fit, but for others it may be too aggressive even with a strong income. The deciding factors are total debt, other essential expenses, and the full cost of ownership, not salary alone.

What percentage of income should go to a car payment?

A practical consumer guideline is around 10% to 15% of gross monthly income, with anything above that becoming more of a stretch. TransUnion also notes that some lenders use PTI limits of 15% to 20%.

Does income affect your credit score?

Generally, no. Equifax says income is not usually used to calculate credit scores and is not included in your credit report, although lenders may still consider income when reviewing a credit application.

What should I include in my car budget besides the payment?

TransUnion says to include taxes and fees, registration, gas, insurance, maintenance, tolls, parking passes, and tickets.

Conclusion

Income should be the starting point for car affordability, not the final answer. The better framework is to look at income, credit score, DTI, PTI, and full ownership costs together. That is the lens supported by both TransUnion’s consumer guidance and Equifax’s affordability messaging.

So, can a $100,000 salary support a $1,000 car payment? Sometimes, yes. But not automatically, not safely for everyone, and not without looking at the rest of the household budget first. The smartest buyers do not ask only, “Can I qualify?” They ask, “Does this payment still make sense after every other obligation is accounted for?”

Latest Posts

Ready to Take the Wheel? Explore Leasing Options

Lease by Model

Lease by Make

Lease by State